Environment

What are the main sources of US greenhouse gas emissions?

Property insurance in the US is getting more expensive and, in some cases, harder to obtain, according to a 2023 Congressional Research Service (CRS) report.

The report links the rising prices and limited access to three main causes:

Public data on how much Americans are spending on property insurance is limited.

According to the Office of Financial Research, the property and casualty insurance industry in the US has struggled in recent years, experiencing industry-wide losses every year from 2017–2022 except for one.

In March 2024, Treasury Secretary Janet Yellen suggested that consumers are dealing with consequences: “Americans across the country are seeing the affordability and availability of their insurance policies decline as a result of increasingly severe climate-related disasters.”

That month, the Treasury Department launched a project in partnership with state insurance regulators to collect more data on how climate risk is impacting insurance markets.

You are signed up for the facts!

The CRS says costlier property damage from natural disaster is due to:

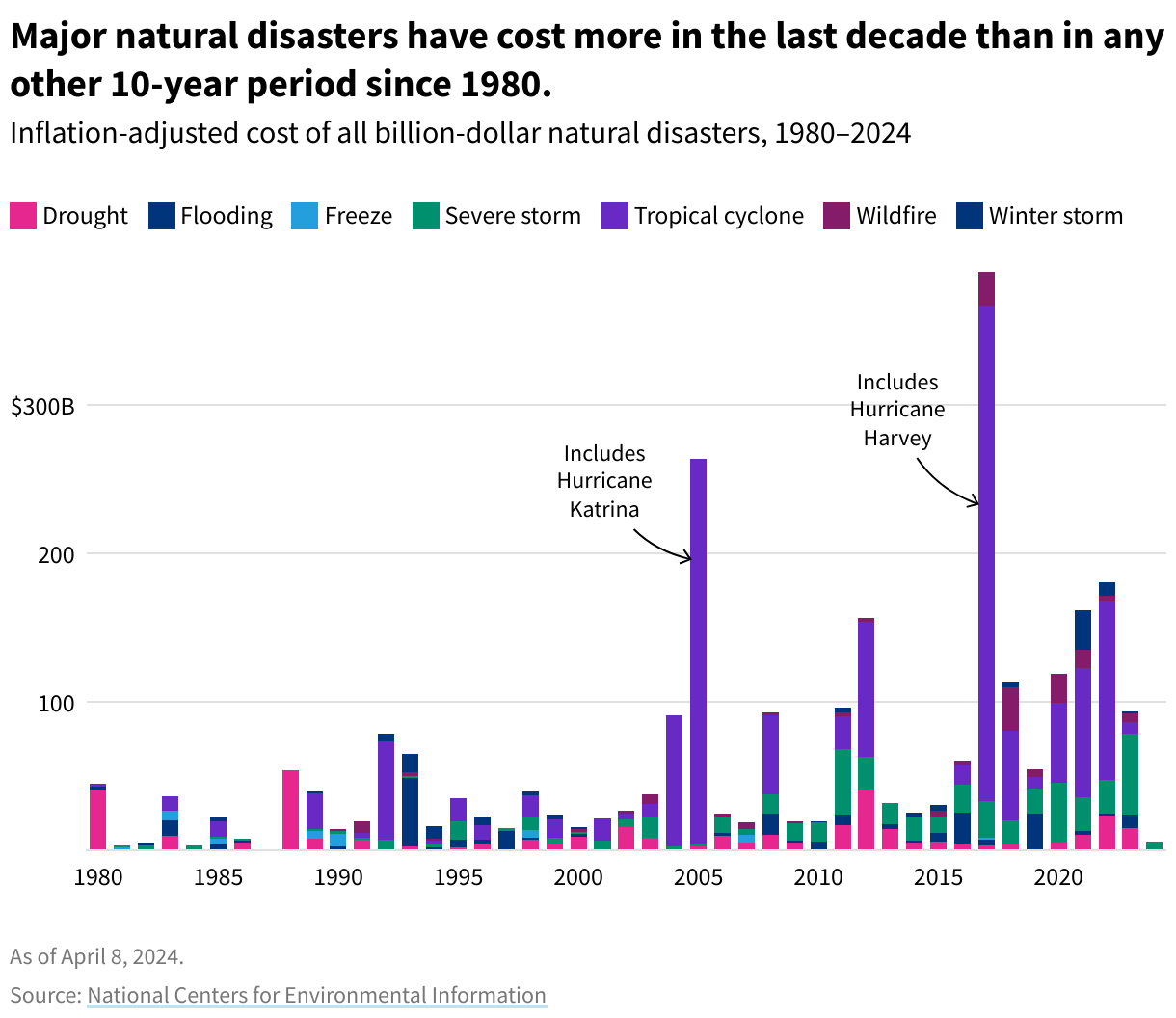

USAFacts has compiled data from the National Oceanic and Atmospheric Administration on the increasing frequency and cost of major natural disasters such as hurricanes, floods, wildfires, droughts, and winter storms. The average cost of these events has been higher over the last 10 full years than in any other 10-year stretch for which data is available.

As the risk of damage from a natural disaster increases, insurance providers are responding by raising premiums or restricting coverage.

In some states, insurance providers have limited their business or pulled out altogether. In California, seven out of the top 12 property insurance providers have paused or restricted new policies since 2022. In Florida, some private insurers have become insolvent and left the market, necessitating a state-operated alternative called Citizens Property Insurance Corporation. In 2023, the US Committee on the Budget launched an investigation into the solvency of Citizens.

In the absence of more comprehensive public data, the National Flood Insurance Program (NFIP) provides an example of how increased losses from climate events are putting insurance programs at risk. The NFIP is a public insurance provider operated by the Federal Emergency Management Agency (FEMA) and designed to insure Americans specifically against flood damage.

According to FEMA, shifts in weather patterns have increased flood risks in recent decades, causing NFIP to suffer losses and accumulate billions of dollars of debt. According to the CRS, NFIP went from debt-free in 2004 — the year before Hurricane Katrina — to $20.5 billion in debt in 2024, even after $16 billion of debt was cancelled in 2018.

The NFIP uses premiums to cover the interest on its debt to the US Treasury, not to make a profit. However, FEMA has stated that the program’s sustainability is questionable without changing that practice.

In recent years, NFIP premiums have increased in cost at higher rates than inflation, rising between 6% and 12% each year from 2015 to 2021.[1]

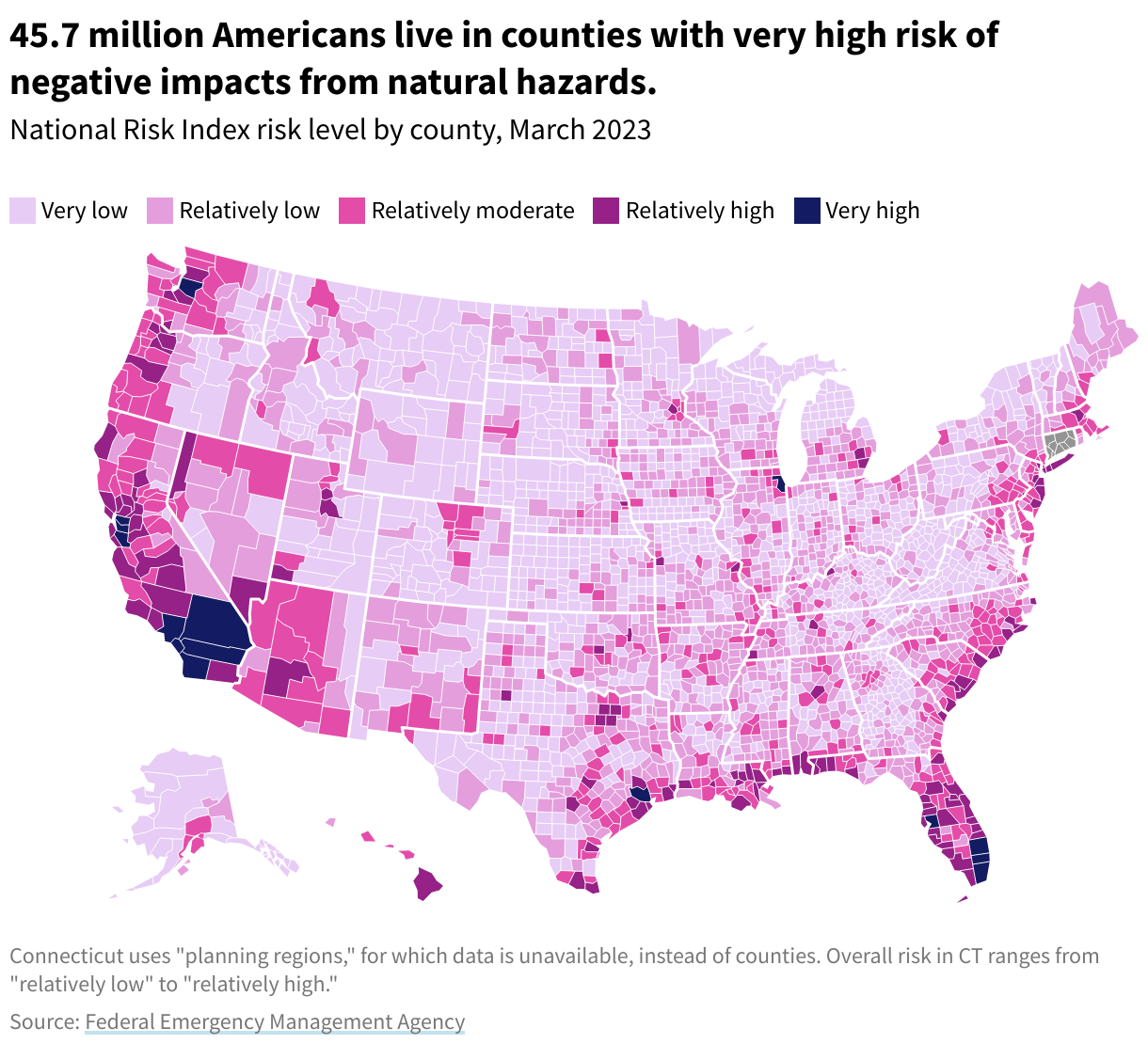

The threat of property damage from natural disasters persists throughout much of the nation. FEMA maintains a National Risk Index assessing the regional risk of damage incurred from 18 different natural causes. The index considers the likelihood of these hazardous natural events, the vulnerability of the population, and the community’s capability to prepare for and respond to the hazards.

According to the National Risk Index, approximately 45.7 million people, or 13.8% of the US population, live in counties with very high risk. Another 86.8 million, or 26.2%, live in areas with relatively high risk.[2]

Major population centers with very high overall risk include:

Learn more about natural disaster insurance and get data directly in your inbox by signing up for our newsletter.

FEMA changed the NFIP pricing methodology in 2022.

Data is not available for US territories.